In a lifetime, the average household in Britain pays over £825,000 to the taxman.

Look at how much tax you’ve ALREADY been forced to hand over to HMRC:

- Your wages are taxed by up to 45%…

- Any profits you make from investing – they’re taxed 25%…

- When you buy a house the stamp duty is as much as 13%…

- Whenever you drive your car you pay road tax…

Then there’s council tax, National Insurance, the list goes on and on. And then when you die, the things you’ve already paid tax on are taxed again. Worse still, it’s your family who has to foot the bill in the event of your death.

No one likes the thought of their relatives being chased for money after they’ve gone. But the only way to ensure the taxman can’t get his mitts on your assets after you’ve passed is to get your affairs in order NOW.

For many, the realisation that they’ll face a problem with Inheritance Tax (IHT) is something that creeps up on them. Often, it’s too late in life for them to do anything about it, which can lead to a nasty surprise. And the shocking truth is, here in Britain, we’re among the worst off on the entire planet when it comes to IHT.

In fact…

Britain is the fourth most expensive place to die on Earth…

You might have thought that a hefty IHT bill was par for the course whatever country you live in. It’s not. In China, India, Russia, Sweden and even Australia your estate isn’t taxed at all. And your kids don’t have to pay a penny after you’ve gone. Even in places like Italy and Austria the amount they’re liable for is an absolute pittance – compared to what we have to cough up here in Britain. And I should know… My parents have moved to Austria and Australia largely to sidestep IHT.

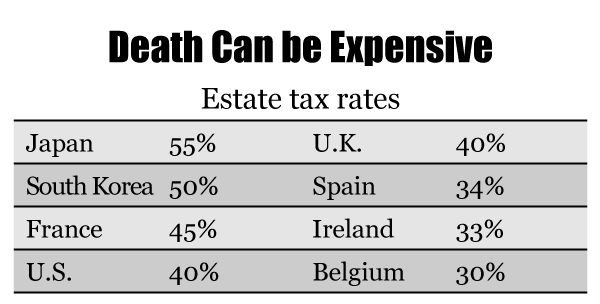

source:taxfoundation.org

As you can see from this table, only three countries on Earth pay more IHT than Britain: Japan, South Korea and France.

I don’t know about you, but it makes me feel like we’re being robbed blind! Is it fair? No. Can you do something about it? Yes. But you need to put a long-term plan in place, beginning right away.

I don’t know about you, but it makes me feel like we’re being robbed blind! Is it fair? No. Can you do something about it? Yes. But you need to put a long-term plan in place, beginning right away.

As part of Britain’s largest underground investment research network, I want to show you EIGHT ways you can protect what’s rightfully yours.

Some of the things you’ll read about in your exclusive report require immediate action. The longer you wait, the less chance you’ll have to use them to your advantage. This isn’t something that you can sit back, forget about and just hope it’ll work itself out. That won’t fly. Your family WILL pay the price, if you fail to act, it’s that simple. But follow the ideas in your report closely, and your children may never worry about having to pay a single penny to HMRC after you’ve gone.

In a moment I’ll show you how to claim your copy, but first, let me ask you a question…

Do you want to be clobbered by HMRC… or leave your wealth to your loved ones?

It should be an easy one for you – or anyone in Britain – to answer. But the figures tell a different story…

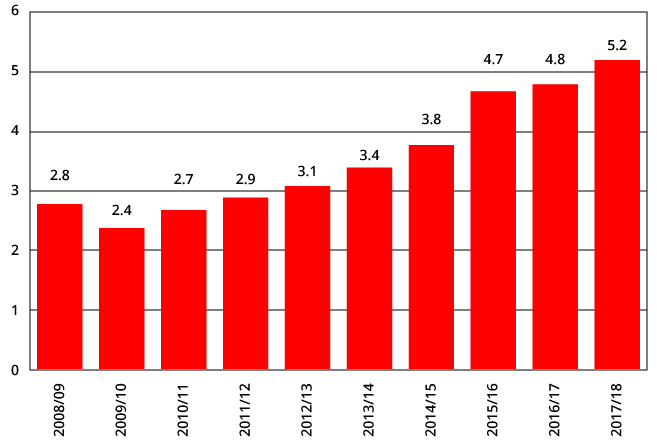

We’re paying more Inheritance Tax in Britain than ever before. In fact between 2000-2018 the amount has more than doubled and as you can see from this chart, since the financial crisis in 2008, it’s absolutely sky-rocketed:

(Source: Statista)

(Source: Statista)

More people are leaving their estate to the taxman, and not their loved ones. Between 2010 and 2017, the number of families paying IHT in Britain is up 160%. By 2020 it’s forecast to nearly double again.

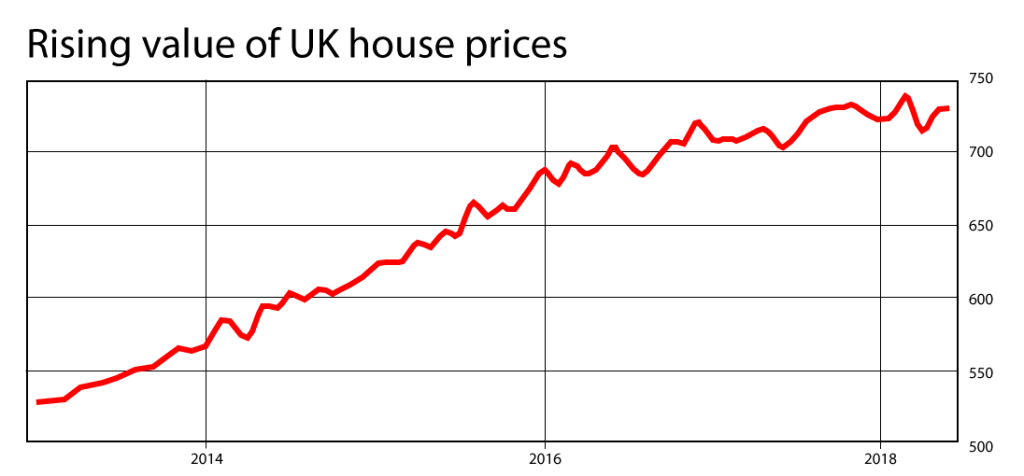

In the last year we paid £5.2 billion in IHT to the taxman – a record. By 2022 it could be as much as £6.5 billion! And this chart below reveals why. The rising value of property in the UK is pushing more and more people above the IHT threshold:

Their assets are at the mercy of the taxman. Maybe yours are too? But they needn’t be.

So…

Let me show you how to turn this situation to your advantage…

Your family can prosper from your estate after you’ve gone. There’s one simple move you can make TODAY that will ensure your kids will never have to worry about covering an IHT bill in the event of your death.

It’s the first thing you’ll discover in your report, titled:

It’s something you probably won’t have thought about before. You probably won’t read about it in the mainstream financial press either…

- It DOESN’T involve investing in stocks…

- It DOESN’T involve setting up a trust…

- It has NOTHING to do with property…

- You DON’T need to “gift” anything to anyone…

- And you DON’T need to change your marital status or anything significant like that…

In fact, this is something that you can do easily today – in no more than a couple of hours. It’s not overly complicated. It’s 100% legal, and it’s ethical. It’s not even a loophole. It’s just something many people don’t know about. And I want to get you up to speed right away – because, without giving too much away here – the sooner you can act, the better.

In your exclusive report, I’ll reveal all along with seven other steps you can take to ensure this whole situation plays out favourably for you and your family.

Click here to find out more about how to protect your family from the taxman when you’re gone.

Nick Hubble

Editor, Capital & Conflict

Important Risk Warnings:

Before investing you should consider carefully the risks involved, including those described below. If you have any doubt as to suitability or taxation implications, seek independent financial advice.

General – Your capital is at risk when you invest, never risk more than you can afford to lose. Past performance and forecasts are not reliable indicators of future results. There is no guarantee dividends will be paid. Bid/offer spreads, commissions, fees and other charges can reduce returns from investments.

Overseas shares – Some recommendations may be denominated in a currency other than sterling. The return from these may increase or decrease as a result of currency fluctuations. Any dividends will be taxed at source in the country of issue.

Funds – Fund performance relies on the performance of the underlying investments, and there is counterparty default risk which could result in a loss not represented by the underlying investment. Exchange Traded Funds (ETFs) with derivative exposure (leveraged or inverted ETFs) are highly speculative and are not suitable for risk-averse investors.

Bonds – Investing in bonds carries interest rate risk. A bondholder has committed to receiving a fixed rate of return for a fixed period. If the market interest rate rises from the date of the bond’s purchase, the bond’s price will fall. There is also the risk that the bond issuer could default on their obligations to pay interest as scheduled, or to repay capital at the maturity of the bond.

The Financial Conduct Authority does not regulate certain activities, including the buying and selling of commodities such as gold, and investments in cryptocurrencies. This means that you will not have the protection of the Financial Ombudsman Service or the Financial Services Compensation Scheme.

Taxation – Profits from investments, and any profits from converting cryptocurrency back into fiat currency is subject to capital gains tax. Tax treatment depends on individual circumstances and may be subject to change.

Investment Director: Boaz Shoshan. Chief Strategist: Nick Hubble. Editors or contributors may have an interest in shares recommended. Information and opinions expressed do not necessarily reflect the views of other editors/contributors of Southbank Investment Research Limited. Full details of our complaints procedure and terms and conditions can be found on our website www.southbankresearch.com.

Zero Hour Alert is issued by Southbank Investment Research Limited.

Southbank Investment Research is authorised and regulated by the Financial Conduct Authority. FCA No 706697. https://register.fca.org.uk/.

Capital and Conflict is published by Southbank Investment Research Limited.

© 2018 Southbank Investment Research Ltd. Registered in England and Wales No 9539630. VAT No GB629 7287 94. Registered Office: 2nd Floor, Crowne House, 56-58 Southwark Street, London, SE1 1UN.