On Monday 5th February, America’s Dow Jones index and the FTSE 100 began a 10% fall.

As it was happening, Tim called me to say that the selling had “lit the touch paper” on the next market crash.

If you have ANY money in the stock market – either directly or through your pension – then please read this letter immediately.

Nick O’Connor, Publisher, Southbank Investment Research

February’s 10% stock market correction fired the starting gun on a potentially ruinous cycle.

But if that sell-off had you spooked, be warned… the real crash is yet to come.

The plan I’ve detailed in this letter is your best chance of keeping your wealth growing… while the unsuspecting suffer a potential 50%+ LOSS.

Could you recover from an 80% hit to your wealth?

Most people couldn’t. It takes years to recover from that sort of loss.

Whatever you’re investing for – whether it’s your retirement, to buy a house, to pay for your children’s education – losing that much money is simply not an option.

Well, it’s the harsh reality for some people.

While February’s sell-off saw 10% wiped off the value of the Dow Jones…

The LJM Preservation and Growth Fund lost 80% of its value.

“Preservation and Growth”!

Their investors thought they were investing their savings in a “low risk” strategy.

They will not be bailed out by the government. That money is gone for good.

And here’s the thing: this wasn’t even a full scale crash… it was just a correction…

And I have no doubt that the biggest losses are yet to come.

So if you have a significant amount of your wealth in the FTSE, I am urging you to reduce it immediately.

My worry is that most private investors will see that the FTSE 100 is going back up again and think that now is a good time the invest – to “buy the dip”, as the saying goes.

As I’ll explain in this letter, that could be one of the riskiest things you could do with your money right now.

This temporary pullback has done nothing to make the FTSE safer.

In fact, I believe the risk to investors has gone UP.

I manage over £100 million in client capital, and I openly declare that only a very small proportion of that money is exposed to US and British stocks.

I’ll show you how I am suggesting you should keep your money growing shortly.

First, it’s imperative you understand why the stock market has just become a whole lot riskier for your money…

Fear is back

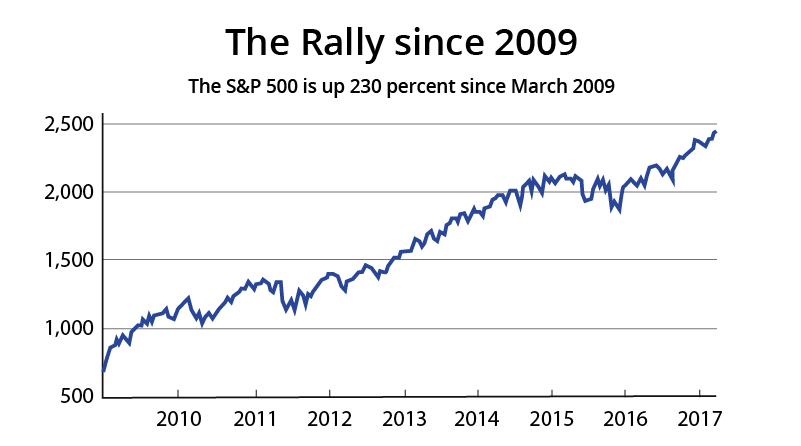

The stock market had been on a historically steady rise since 2009, prior to February’s sell-off.

The FTSE 100 more than doubled…

The S&P 500 almost quadrupled.

The Volatility Index (VIX) – which indicates whether investors believe stocks are heading up or down – broke new ground in optimism.

Before February’s sell-off, investors had seemingly forgotten prices could go down.

The VIX – known colloquially as the ‘fear index’ – went to record lows as the S&P 500 rose throughout 2017:

The lowest the VIX had ever reached before the financial crisis was 9.89, in January 2007.

In July 2017, the VIX went UNDER 9 for the first time ever.

On 3rd January 2018, it did so again.

Investors had never been so sure the stock market would keep rising…

They were wrong.

Increased volatility is going to cost investors trillions of pounds

Here’s the thing…

When the big players – banks, pension funds etc. – invest their clients’ money, volatility is a critical factor in picking the right investments.

A pensioner, for example, doesn’t want to see their wealth swing up and down by +/-20%.

They can’t afford to take on unnecessary risk – they just want a steady rise.

That’s why institutional investors are required to have the bulk of their portfolios in low-volatility assets…

And they use past volatility to assess how “safe” an investment is.

Here’s the problem…

Due in large part to the regular supply of printed money (quantitative easing) central banks have injected into the stock market since 2009, the bull market had been incredibly smooth.

I.e. volatility has been LOW, as you can see on this chart of the S&P 500:

Source: Google Finance

After all, why would you sell your stake in a market you knew the central bank was propping up?

Central bank money printing (Quantitative Easing) has sent markets into a self-perpetuating cycle, driving them up and up and up.

The S&P 500 even completed a record-breaking stretch of more than 400 DAYS without a drop of more than 5% – the longest streak since the 1950s…

Volatility had never been lower.

The normal price fluctuations you’d expect to see had been suppressed.

Investors had never been so optimistic…

But on February 5th, when the Dow Jones fell by over 1,000 points…

Volatility returned.

The critical lesson from the global stock sell-off

The bull market has essentially been a years-long trap for investors.

But February’s correction has called time on the unprecedented low levels of volatility.

The game is now up – and that could have huge consequences for your money.

This is why…

The big institutional investors who dominate the market will now have to factor in February’s HIGH volatility into their risk calculations…

Which could reveal their portfolios to be nowhere near as safe as they thought they were…

Meaning they will have to UNWIND their riskier positions to ensure their clients’ money is safe.

Can you see the problem with this?

Huge financial institutions realise simultaneously that their portfolios are too RISKY for their clients…

Meaning they have to SELL some of their positions to make them safer.

If they all do this at once…

You’ll see a glut of stocks hit the market in one go.

That’s all the ingredients necessary for a stock market crash, right there.

In my view it’s not hard to see the sell-off destroying more wealth than we saw in 2008 – when this exact same mistake was made, prompting the FTSE 100 to fall 50%.

But due to almost a decade of Quantitative Easing since 2008 – the European Central Bank is still pumping 60 billion euros a month in the markets – this problem will be dramatically bigger now.

It’s a recipe for chaos – which is why, if you have ANY money in western stock markets, I’m advising you to take steps to protect yourself immediately.

As Andre Bakhos, managing director of New Vines Capital, said to Reuters in response to the February correction [emphasis mine]:

“The one thing I could say with confidence is that volatility has suddenly come back into the market.

“The volatility has caused investors to be fast on their feet. It is a true traders’ atmosphere as opposed to the conditions we have been accustomed to – buy and go higher.”

He’s right.

When stock markets tanked last time, central banks revved up the printing presses, pouring liquidity in the financial system.

This time…

They CAN’T.

The economy is doing too well and inflation is too high already.

I think they’ll have to watch the financial markets going haywire as this “great unravelling” takes hold.

The next move you make is critical.

Get it wrong, and I believe you could lose well OVER 50% of your money.

February’s sell-off is going to split investors into two camps:

- Those who believe it was a momentary “blip” and that the bull market will continue as it was beforehand…

- Those who understand that volatility is back… who understand that investors have been lulled into a false sense of security for almost a decade… and the threat a GREAT UNRAVELLING poses to your money.

My message to you today is simple… but critical: make sure you’re in the second camp

I’m offering you an escape route…

Risk Warning

Your capital is at risk when you invest in shares – you can lose some or all of your money, so never risk more than you can afford to lose. Past performance and forecasts are not reliable indicators of future results. Bid/ offer spreads, commissions, fees and other charges can reduce returns from investments. There is no guarantee dividends will be paid.

Profits from share dealing are a form of capital gain and subject to taxation. Tax treatment depends on individual circumstances and may be subject to change in the future.

Investment Director: Tim Price. Editors or contributors may have an interest in shares recommended. Information and opinions expressed do not necessarily reflect the views of other editors/contributors of Southbank Investment Research Limited. Full details of our complaints procedure and terms and conditions can be found on our website, southbankresearch.com.

London Investment Alert is issued by Southbank Investment Research Ltd.

Southbank Investment Research Limited is authorised and regulated by the Financial Conduct Authority. FCA No 706697. https://register.fca.org.uk/.